特朗普2.0的政策目的仍然是「讓美國再次偉大」(Make America Great Again, MAGA),做法是「美國優先」(America First),政策範圍則包羅甚廣。美國甚為保守的智庫傳統基金會(Heritage Foundation)在2023年出版了「2025計劃」(Project 2025)報告,詳細列出不同範疇的政策執行方向。這份長達900頁的報告,有100多個保守主義機構和一些前特朗普政府的官員參與,雖然特朗普口口聲聲說報告和他無關,但可說代表了保守派主流思想。2016年特朗普競選總統時傳統基金會也有類似報告,並認為特朗普首兩年任期內已跟隨該報告的64%建議。

在經濟領域上,特朗普2.0比較確實的政策範圍包括減稅、減少貿易逆差和減少進入美國的移民。特朗普於2017年成功在國會通過「減稅及職位法案」(Tax Cuts and Jobs Act),但其中多項條款只是臨時的,將於本年底失效。若沒有進一步的立法行動,稅率便會在年底回升至之前的水平。

Through the ebb and flow of its economy in the aftermath of the Second World War, Hong Kong has sealed its status as an international financial and trade centre on the world’s economic stage. However, in light of the global economic downturn, fierce regional competition, and worsening geopolitical situation in recent years, coupled with the fact that Hong Kong–as a highly externally-oriented free economy–cannot afford to be complacent simply because it has historically managed to turn crises into opportunities. Times have changed. Now beleaguered by internal problems such as an ageing population as well as external challenges, the city may no longer be as “hardy” as it once was.

To address the challenges in the new era, Hongkongers should not stick to the old rut and must find ways to enhance competitiveness so that long-standing and thorny problems can be resolved.

Formidable problems facing the economy

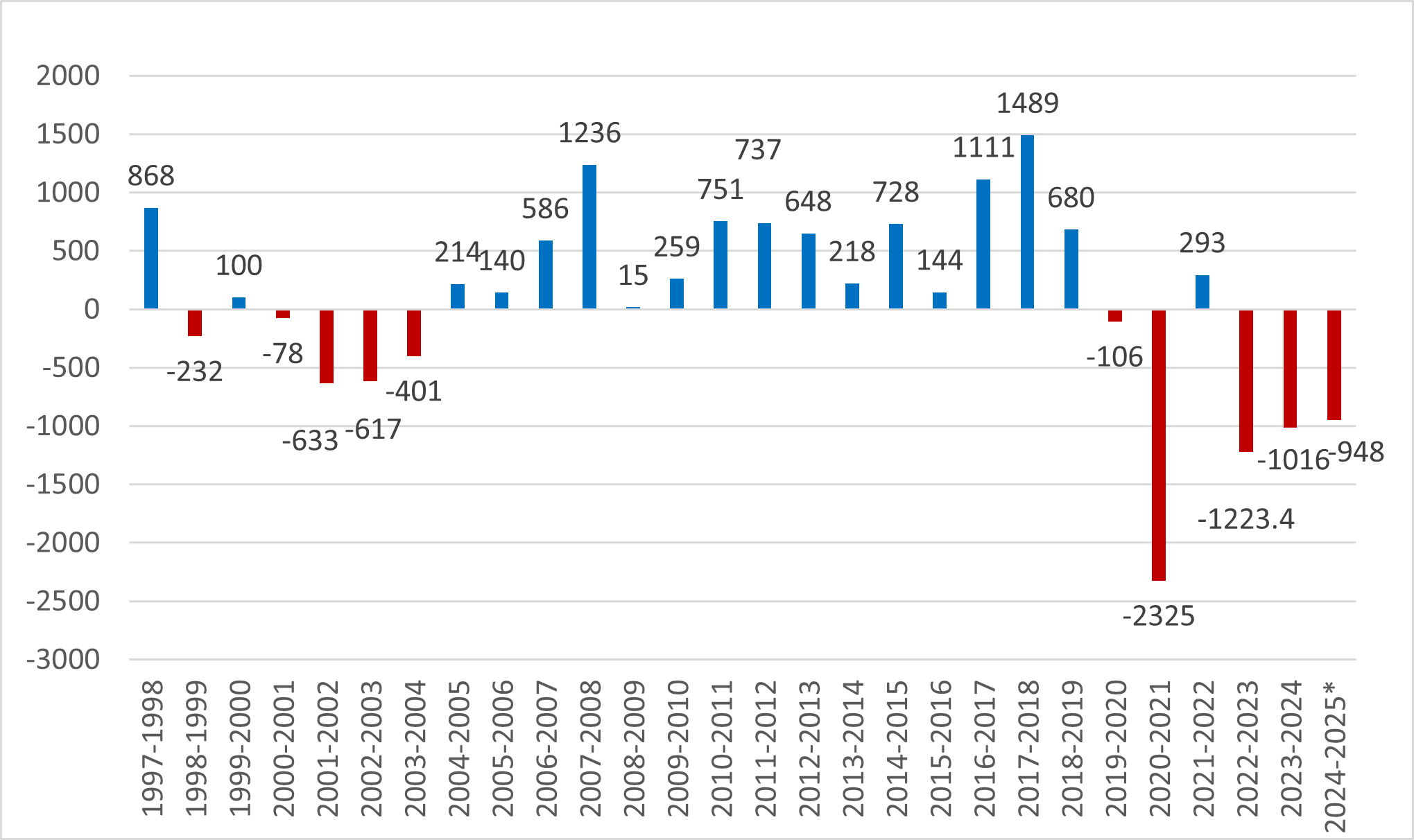

The first challenge facing the Hong Kong economy over the past few years is the SAR Government’s persistent fiscal deficits. After racking up a record-high surplus of $149 billion for 2017–18, the Government registered a fiscal deficit of $100.2 billion for 2023–24. Initially projected to be downsized to $48.1 billion for the current year 2024–25, the deficit is now estimated to reach $100 billion. Barring the reduction in income from Government-issued bonds, the actual deficit would be even larger. Factors underlying the deficits include fast-increasing government expenditures as well as decline in government revenues. Government expenditure soared significantly from $470.9 billion for 2017–18 to $721.3 billion for 2023–24, of which non-recurrent, social welfare, and healthcare expenditures grew the fastest. The last two items are unlikely to be cut. Meanwhile, government revenue dropped from $619.8 billion to $549.4 billion.

The Figure shows that in 2017–18, 26.6% of the Government’s main sources of revenue came from land premium while 15.4% came from stamp duties. In 2023–24, the share of land premium plummeted to 3.6% and stamp duties dramatically slumped to 8.9%. Despite seeing its share rise from 3.5% to 13.6%, investment income is, after all, not a stable source of revenue. In addition, the Inland Revenue Department annual report 2023–24 reveals that in the year of assessment 2022–23, only around 1.83 million people were required to pay salaries tax, which means that the tax base is still narrow. Given the overall economic downturn, it is unlikely that the Government will be able to sharply reduce the persistently-high fiscal deficits in the short run.

Figure Sources of the Hong Kong SAR Government revenue for 2017–18 and 2023–24

The second challenge facing the Hong Kong economy is the failure to fully leverage the economic benefits from the integrated development of the Guangdong-Hong Kong-Macao Greater Bay Area (GBA). Despite the high degree of integration of consumption activities in the GBA, Hong Kong’s professional services sector has yet to be fully integrated into the development of the GBA. While it has become a trend among Hongkongers to go north for spending, there is much less incentive for Mainlanders to spend in Hong Kong. At the same time, more and more local people prefer to shop on Mainland e-commerce platforms, inevitably impacting the sales of physical stores in Hong Kong. According to the Census and Statistics Department’s data, the Value Index of Retail Sales dropped from 144.8 points in 2018 to merely 121.3 points in 2023 while the monthly average for the first 10 months of 2024 went further down to 111.8 points.

Furthermore, the Volume Index of Retails Sales dropped from 148.9 points in 2018 to 113.9 points in 2023, and even averaged 103.3 points in the first 10 months of 2024. The decreases for both indexes are equally significant. Due to constraints in rent and labour costs, the local retail industry can hardly compete with its Mainland counterpart in terms of cost-effectiveness. It seems that the professional services industry, in which Hong Kong excels, has not been able to capitalize on the market opportunities in the GBA. This can be put down not only to the sluggish macroeconomy in recent years but also to delayed cross-boundary professional qualification certification, administrative red tape, and other factors.

The third challenge facing the Hong Kong economy is the gradual shrinking of the middle class and international talent drain. Hong Kong’s unitary economic structure is one of the primary reasons for the weakening middle class. Since middle-income jobs have always been concentrated in the financial, real estate, and professional services industries, problems will start to surface as soon as these sectors face headwinds. In addition, while there has been a mass migration of middle-class families overseas in the last few years, the highly-educated new immigrants to Hong Kong are less internationalized. The LinkedIn profile data analysed in an essay in the “Hong Kong Economic Policy Green Paper 2024” published by the HKU Business School demonstrates that the proportion of Asians among leavers is 58% and is as high as 79% among joiners, while the number of connections of leavers is 1.7 times that of joiners.

Four reform strategies to chart a new course

Cracking the above problems is no easy task. Let me outline below four policy directions to spark more valuable ideas from all sectors.

Broadening the tax base to tap new revenue sources

Hong Kong can take a leaf from Singapore’s book and consider introducing consumption tax progressively to relieve financial pressure on the Government. The goods and services tax (GST) implemented in Singapore at a rate of 3% in 1994 gradually rose to 9% in 2024. In 2023, the GST contributed to 15.7% of Singapore’s fiscal revenue. Based on private consumption expenditure in Hong Kong, and after deducting existing overlapping tax items, a 2% GST can bring the Hong Kong SAR Government an incremental income of $27 billion, roughly equivalent to 5% of the financial revenue in 2023. Referencing Singapore’s experience, retail sales fell following upward adjustments of GST in 2007 and 2023, but not after GST hikes in 1994, 2003, and 2004. An economist at RHB Bank points out in a recent study that the GST increase in January 2024 did not have a strong impact on Singaporeans’ spending habits. This suggests that a GST rise does not necessarily dampen retail sales. The key lies in a balanced measure that entails controlled tax increases, effective expectations management, and complementary welfare policies to maintain steady consumer sentiment.

As a matter of fact, the introduction of GST in Singapore did arouse controversy. For example, there were views that daily necessities should be exempted. The Singaporean government did not accept this suggestion because of the potential increase in compliance and audit costs. Instead, the authorities chose to alleviate pressure on low-income families by issuing GST vouchers, subsidizing public education and healthcare services, etc. In any case, if the GST rate is set too low, it will not be adequate to alleviate the Government’s financial problems. Conversely, if the rate is set too high, it will breed dissatisfaction among businesses and the general public and could build up excessive inflationary pressure. How to strike a balance in between is a great challenge for policy formulation. Moreover, the Government can consider selling idle assets, including unused premises and surplus equity, to ease financial pressure.

Fostering development via public-private partnerships

The SAR Government can consider strengthening public-private partnerships to promote infrastructure development. Apart from reducing the Government’s initial investment and operating costs, this approach helps to bring in technologies and management experience from leading enterprises. Many international cities have achieved remarkable results through this development mode. Examples include the Chicago Skyway and the Port of Long Beach Middle Harbour Redevelopment Project in the US, the Marina Bay Sands Integrated Resort in Singapore, the Beijing subway Line-4 project, and the Eastern Harbour Crossing in Hong Kong. There are, of course, different forms of public-private partnerships, with “Build, Operate, and Transfer”; “Build, Own, and Operate”; “Transfer, Operate, and Transfer” among the most common modes. Hong Kong can choose the suitable mode depending on its specific needs.

Leveraging unique advantages to integrate into the GBA

Hong Kong needs to optimize its integration with other cities in the GBA to give full play to the benefits of the regional economy. According to the Second Agreement Concerning Amendment to CEPA Agreement on Trade in Services recently signed by the SAR Government with Mainland authorities, the Mainland market will be further opened up to Hong Kong enterprises offering professional services. On this basis, the SAR Government can continue to maintain close liaison and cooperation with other GBA cities to ensure the successful implementation of policies. For instance, assistance can be provided for Hong Kong’s estate surveying companies to complete the filing of records to bid for consultancy services projects in joint ventures within the GBA.

Given the distinct advantage of Hong Kong’s higher education in the GBA, the SAR Government can maintain close cooperation with sister cities and continue to support higher-education institutions in building branch campuses in the GBA and achieving success in their subsequent development. Opening up the “four flows”―human flow, goods flow, capital flow, and information flow―is of vital importance in this regard. Only by doing so will it be possible for the branch campuses in the GBA to obtain invaluable resources from both the Mainland and abroad, and for Hong Kong’s higher education institutions to preserve their competitive edge in internationalization.

To maximize the removal of operating restrictions on Hong Kong’s professional service sectors, such as finance, law, and accounting, in the GBA, the SAR Government needs to continue to lift systemic barriers in the area. For example, in the First Phase Report on Survey of the Current Situation of Hong Kong Legal Practitioners under the Development of the Guangdong-Hong Kong-Macao Greater Bay Area, the Law Society of Hong Kong and the School of Law of Sun Yat-sen University point out that under Mainland laws, the associations formed by Hong Kong law firms with Mainland law firms shall not be in the form of partnership or legal entity. Therefore, cooperation between Hong Kong and Mainland law firms is mainly based on non-partnership associations. This gives rise to various problems, including differences in handling conflicts of interest, discrepancies in business acceptance and processing standards, and a lack of clarity on the legal responsibilities of non-partnership associations.

Proactively competing for talent and enticing foreign investments

Apart from talent and capital from the Mainland, Hong Kong must also focus on attracting talent and funds from abroad to maintain its relative advantages as an international metropolis. In view of the fact that the career development of ethnic Chinese technology experts in Europe and the US is thwarted by current geopolitical tensions, the SAR Government should seize this opportunity to encourage them to advance their careers in Hong Kong. Meanwhile, the authorities can also consider setting specific performance indicators for local universities, e.g. target percentages for international students, to reinforce local higher education institutions’ strengths in internationalization.

Needless to say, Hong Kong must continue to leverage the unique advantage of “one country, two systems” to draw in more direct foreign investments to the Mainland. At the same time, apart from enticing Mainland investments through the Government’s Office for Attracting Strategic Enterprises, it is also necessary to enhance the presence of leading foreign enterprises to maintain Hong Kong’s distinctive advantage as a bridge to the world. The growth of emerging sectors, e.g. artificial intelligence, biotechnology, financial technology, advanced manufacturing, and new energy sources, will determine if Hong Kong can produce more high-quality jobs in future, thereby expanding its middle class and furthering its economic prosperity.

As we mentioned in this column two years ago, priority should be given to creating a liveable environment when it comes to attracting talent. Otherwise, they will not stay after arriving. On the one hand, they need to find high-quality jobs in Hong Kong, connect with a thriving professional community, and enjoy a comfortable and vibrant living environment. On the other hand, high-quality human capital is a key consideration for companies with an eye to establishing their presence in Hong Kong. Hence, efforts to attract companies and capital, compete for talent, or even formulate cultural policies should be complementary rather than isolated from one another. Retaining talent and businesses is a systemic project that requires comprehensive policy coordination across the SAR Government to achieve success.

Nowadays, with the advancement of artificial intelligence (AI) technology in leaps and bounds, AI applications have permeated various aspects of human life—not only from smart assistants to autonomous driving technologies but also from industrial production to medical diagnosis. According to the International Data Corporation, the global AI market value is expected to rise from US$132.4 billion in 2022 to US$512.4 in 2027.

While the convenience of AI innovation is applauded by all sectors of society, does it also raise the community’s awareness that the technological revolution is subtly exerting a tremendous impact on the global environment? As a matter of fact, the problem of carbon emissions arising from the AI development process has reached such a state that it can no longer be ignored.

The invisible killer: the carbon footprint of AI training

To understand the impact of AI on the environment, it is necessary to unveil the true face of AI training models. The training process for modern AI models, particularly large language models, requires massive amounts of data and calculation resources. The latest research by the University of Massachusetts Amherst indicates that carbon emissions from training a large AI model can reach 626,000 pounds, equivalent to the total emissions from five vehicles throughout their entire life cycle, from production to disposal.

Specifically, approximately 552 tonnes of carbon dioxide are emitted during the training process of GPT-3 while the CO2 emitted from training the even larger model, GPT-4, is estimated to exceed 1,000 tonnes. Of particular concern is that these figures continue to go up. Under the sectoral consensus that “large models are the order of the day”, giant technology companies have been vying to develop even larger models, resulting in exponential surge in energy consumption. The AI sector’s carbon emissions are forecast to account for 3.5% of the world’s total carbon emissions by 2030.

Data centres: an energy-guzzling beast in the AI era

The energy consumption of large AI models has now reached an alarming level. Data of the Stanford AI Laboratory shows that one single training session of GPT-3 typically uses 1,287 megawatt-hours of electricity, equivalent to all the power consumption of 3,000 Tesla electric cars each travelling 200,000 miles, emitting a total of 552 tonnes of carbon dioxide.

In daily use, every response generated by ChatGPT requires 2.96 watt-hours of electricity, almost 10 times that (0.3 watt-hour) for a standard Google search. Each Google search powered by AI even utilizes 8.9 watt-hours. The water resource consumption level is also alarming. During its training, GPT-3 consumes close to 700 tonnes of water. For every 20 to 50 questions, 500 millilitres of water are required. For cooling of its data centres alone, Meta used over 2.6 million cubic metres of water in 2022.

Root causes of escalating energy consumption

The colossal energy consumption of large AI models can mainly be attributed to two core factors. First, the rapid iterations of AI technology have significantly stimulated the demand for chips, directly pushing up electricity consumption. The training and inference processes of modern AI models deploy enormous computational resources, which primarily rely on high-performance hardware, including graphics processing units and application-specific integrated circuits. This hardware is highly energy-intensive when running complex computations. As AI models keep expanding in size, their computational capabilities have seen exponential growth, resulting in an ever-increasing demand for high-performance chips and, consequently, mounting energy consumption.

Furthermore, substantial computational power is essential for supporting the AI model training process. The around-the-clock data centres generate excessive heat, necessitating cooling treatments. Energy consumption is an especially severe issue for data centres, which serve as the core infrastructure for AI computation. Servers and storage devices running at high loads release a vast amount of heat. If the heat is not dissipated in time, both the performance and lifespan of the devices will be seriously compromised. Hence, data centres are equipped with super-efficient cooling systems to ensure that the devices operate at optimal temperatures.

In the operating cost structure of a data centre, electricity tariffs account for 60% of the total cost, of which over 40% is spent on cooling systems. At an air-cooling data centre in particular, more than 60% of electricity is used for cooling while less than 40% is used for computation. As a result of this energy utilization imbalance, the energy consumption of data centres around the world is now almost 10 times more than it was a decade ago. Traditional air-cooling systems are less costly but also less efficient, making them incapable of meeting the requirements for high-efficiency cooling. In comparison, except for a large-scale investment at the initial stage, liquid-cooling systems are more efficient, thus sharply reducing energy consumption at data centres.

In addition, the site selection and design of data centres have a significant impact on energy consumption. Many data centres are located in areas with lower electricity costs but in hot climates, placing a heavier burden on the cooling systems. To enhance energy utilization efficiency, priority should be given to locations with cooler temperatures and a stable energy supply. Besides, a modular design should be adopted so that resource allocation can be flexibly adjusted according to needs.

Finally, the training and inference processes of AI models also involve huge amounts of data transmission and storage, which inevitably boost energy consumption. As more and more data is created, data centres need extra storage devices and greater bandwidth to cope, which further expands energy consumption. These facts demonstrate that companies should make use of data compression and transmission optimization technologies to cut down energy consumption by minimizing unnecessary procedures.

Corporate solutions and policy suggestions

In the face of the environmental challenges from AI technology, companies and policy-makers need to take a series of carbon-reduction measures. First, businesses should maximize the use of green energy and energy-saving technologies. Investments should be made in renewable energy sources such as solar energy and wind energy to minimize reliance on traditional fossil fuels. Second, enterprises should optimize AI model training algorithm to streamline computation, cutting down energy consumption at source. Third, they should enhance data centre management and upgrade technologies; use high-efficiency solutions such as liquid-cooling to promote energy utilization efficiency; and minimize waste of idle resources through smart dispatch and load balancing. Fourth, through virtualization technology, companies can integrate computational resources to lower energy consumption.

In terms of policy-making, the government should first set strict energy efficiency standards and promote green development of AI technology; and, through tax concessions and funding, encourage enterprises to adopt energy-saving technologies and renewable energy sources. Second, regulation of data centres should be strengthened and energy efficiency evaluation standards should be established to promote overall energy efficiency. Third, governments and industry should join hands to spread environmental awareness among the public and businesses. The negative impact of AI technology on the environment can be minimized through such mechanisms as carbon trading and carbon offsets. Both education and publicity are indispensable, as only when the relationship between AI advancement and environmental protection is widely known can a social consensus be reached and concerted efforts be made to address the problems.

Glimmers of hope amid crisis

The trend of AI technology may well be overwhelming, but we must ensure that the environment will not be harmed as a result. Through technological innovation, corporate self-regulation, government guidance, and social oversight, environmental impact can be minimized while the convenience of AI can be enjoyed by all. The International Renewable Energy Agency predicts that, with proactive measures, the annual growth in carbon emissions by the AI industry can be controlled within 5% by 2030.

As witnesses and participants of this era, each and every one of us should be concerned about the environmental issues brought about by advancements in AI and take concrete actions to support its green development. Only through this approach can we ensure that the AI technology benefits mankind instead of becoming another burden on the Earth. In our quest for technological breakthroughs, environmental protection should be the bottom line that must be upheld, not just a token gesture. Let all sectors of the community make concerted efforts to drive AI towards a greener and more sustainable future.

Through policy guidance, technological innovation, and public engagement, the path will be paved for Hong Kong to achieve the AI industry’s carbon-neutral goals by 2035 and contribute to the sustainable development of the world.

When we listen to music through our earphones these days, do we realize that over 30% of it is already produced by AI? Last year, the AI-generated song “Heart on My Sleeve” got 20 million hits on Spotify. Early this year, the burgeoning AI-generated music scene drove Universal Music, the world’s leading music company, to remove all its records from TikTok, the largest platform for short-form mobile videos. After the two companies reached an agreement in mid-2024, TikTok agrees to label all AI music footage accordingly. The impact of AI technology on the music industry has been fast and furious.

Cause for celebration or concern

With the progress in AI technology, major technology companies have extended their reach over the music industry. For example, the text-to-music model named MusicGen was launched by Meta to users in 2023. The Stable Audio 2.0 model, introduced by Stability AI this year, even allows users to upload existing music to generate new tracks in a completely different style. The acoustic quality is comparable to that of a vinyl record.

It is a cause for celebration because AI enables ordinary people, who are not music professionals, to not only “create” music with ease but also earn money from these “creative” works. Boomy, an American start-up, supports users in uploading their AI-generated music to Spotify and other streaming platforms for a commission.

That being said, it is a cause for concern because if music can be “created” by an AI model, would professional musicians find themselves out of a job? Given the five consecutive months of protest from Hollywood actors and screenwriters in 2023, the looming fear is clear as day.

As a matter of fact, the great concern is not unjustified. In 2017, 87% of music tracks played on Spotify were from singers signed with record labels. By 2022, this percentage fell to 75%. As of 2023, over 100 million pieces of music were generated by AI, taking up around 30% of our music-listening time. The revenue generated by the AI music market is projected by industry members to reach US$7 billion by 2026, while AI music is expected to have a 50% share of the music sector by 2030.

Quantity or quality

At present, the advantages of AI-generated music lie in speed and quantity. Boomy claims that in just a few years, there are already 18 million pieces of AI-generated music, whereas only 100 million pieces of old and new music spanning all time periods have found their way to Spotify so far. Nevertheless, does the quality of AI-composed music rival that of the creative works by professional musicians? So far, the works created by AI have been based on past music. With the rapid growth in quantity, the quality of AI-generated music will eventually regress to the mean. When the excitement over this new technology wears off for the public, will people tire of AI-produced music and turn to works by music artists? Alternatively, one wonders if a “scientific division of labour” is possible, whereby AI-generated music serves as low-cost background music while the concert stage is reserved for music artists’ works to shine.

When it comes to people’s requirements for music, quantity and quality are never mutually exclusive. Striking a balance between the two is something that both AI companies and music artists should explore.

As a matter of fact, both music artists and record companies, which rely on music copyrights to survive, are on the receiving end of AI-generated music’s vexing challenge. The music works owned by record companies provide the raw materials for AI models to “create” new music after learning their characteristics. But should AI companies be obliged to pay royalties for these raw materials? And should AI-created music be under copyright protection?

Recent years have seen increasing challenges arising from these issues. In 2023, for instance, Universal Music accused Anthropic, an AI company with investments from Google and Amazon of illegally using works owned by Universal Music to train Anthropic’s AI models. In its defence, the company claims that using existing music to train AI models does not constitute copyright infringement.

Challenge or opportunity

Since advancements in AI technology have far outpaced developments in intellectual-property laws, these problems without quick solutions have become a grey area, presenting both challenges and opportunities for record companies and AI technology companies. In retrospect, this is not the first time music publishers have encountered copyright challenges. The late 20th century saw the migration of music from CDs to electronic MP3 files, which, coupled with the rise of sharing platforms like Napster, led to rampant pirated music that pushed many record companies out of business. It took an entire decade for record companies to develop a business model more profitable than the traditional approach of selling CDs and to eventually reach agreements with music streaming platforms regarding music copyright.

Taking lessons from history and embracing the unstoppable trend of AI music, record companies no longer regard it as an uncontrollable beast. Instead, they are striving to devise a new business model that can enable music copyrights to bring greater profit in the AI era. Robert Kyncl, CEO of Warner Music Group, once says that simply rejecting AI and fighting against it is out of the question. In promoting legal definition and protection of music copyright, record companies actively use AI to facilitate music creation by professional artists in cheaper and faster ways on the one hand. For example, AI is harnessed to produce multilingual versions of podcasts for the enjoyment of audiences around the world. Machine learning has even been used to extract a muddled demo song left behind by the Beatles’ lead singer, John Lennon, in 1973. The recent release not only gave new life to the song “Now and Then” but also reignited enthusiasm for their Beatles’ classic ballads. On the other hand, AI models are also trained to precisely detect copyright-infringing music for litigation purposes, if necessary. Additionally, record companies may even roll out a two-pronged carrot-and-stick strategy to protest against copyright infringement by AI companies while leveraging their advantage as copyright owners to become market pioneers through closer cooperation with AI companies.

Two centuries ago, the Fate Symphony strikes a chord with us, helping us to empathize with Beethoven’s struggle against destiny after losing his hearing. Two centuries later, if Beethoven came back to life, could AI restore his hearing to inspire him to compose even more masterpieces for posterity? Two hundred years ago, through musical notes, Beethoven issued the rallying cry: “Listen! Fate is knocking at the door!” Today, two hundred years later, hopefully the door opened by AI will lead to a new era of human creativity!

根據民調,三分之二的美國選民對經濟給予劣評,收入較低的一群傾向於支持特朗普。2020年,他以15個百分點的差距失去收入介乎5萬至10萬的選民,但在這次選舉中卻逆轉獲勝。民主黨人似乎忽略了馬斯洛的需求層次理論(Maslow’s Hierarchy of Needs):基本需要(如財務穩健和身心健康)必須先行,然後再滿足其他方面。在競選活動中,民主黨聚焦於民主等議題而忽略經濟。曾經是該黨核心的工人階級選民不再予以支持,因愈來愈多人按自身的經濟利益來投票。黨內對敗選結果莫衷一是,更出現互相指摘。如此反應,是否就能把選票贏回來?答案不言而喻。政治指摘伎倆層出不窮,皆因政黨或領導人藉此進行政治操弄,以便大權在握。

指摘別人似乎也具傳染性。2009年,心理學學者David Sherman 和 John Klein發表合著論文【註】,其中一個實驗要求參與者閱讀有關政治失敗的新聞,然後寫下政客的過失。讀到關於政客將失敗歸咎於特殊利益的報道時,參與者更可能將自己的失敗責任推卸給別人。至於讀到政客承擔責任的參與者,則更可能肯為自身的不足負責。同理,管理高層若輕易指摘別人,公司員工也會有樣學樣。如此一來,不難衍生出一種推卸責任的指摘文化。