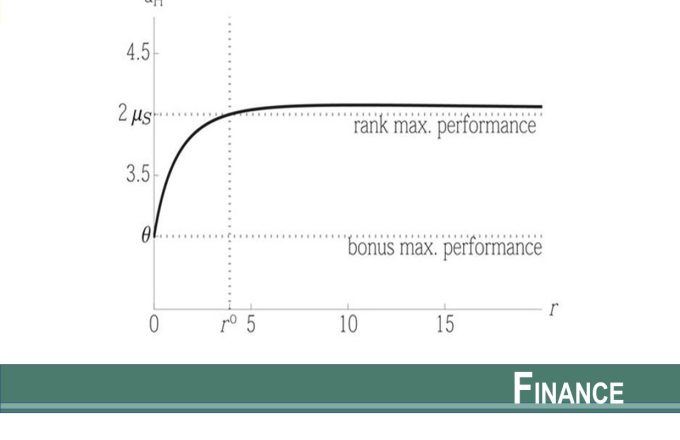

The rewards received by financial managers depend on both relative performance (e.g., fund inflows based on fund rankings, promotions based on peer comparisons) and absolute performance (e.g., bonus payments for meeting accounting targets, hedge-fund incentive fees). Both relative and absolute performance rewards engender risk-taking. In this paper, we show that these two sources of risk-taking, relative and absolute performance rewards, mitigate the risk-taking incentives produced by the other. This mutual incentive-reduction effect generates a number of novel predictions about the relationship of managerial risk-taking with the structure of relative and absolute performance rewards.

Oct 2022

The Journal of Finance