Testing AI in the Real World – HKU Business School Released AI Agents’ Trading Performance

HKU Business School today released the results of a groundbreaking study evaluating how well today’s leading Artificial Intelligence models can perform as independent foreign exchange traders.

Over the past year, AI large language models (LLMs) have rapidly evolved from simply generating text to taking independent actions and using complex tools. However, a key question remains: can these AI agents actually make profitable decisions in real-world, unpredictable environments?

To test this, the Artificial Intelligence Evaluation Lab (AIEL) at HKU Business School, led by Professor Jack Jiang, launched Agentic Trader, through which they evaluated the autonomous trading capabilities of LLM agents in live foreign exchange markets.

Key Findings

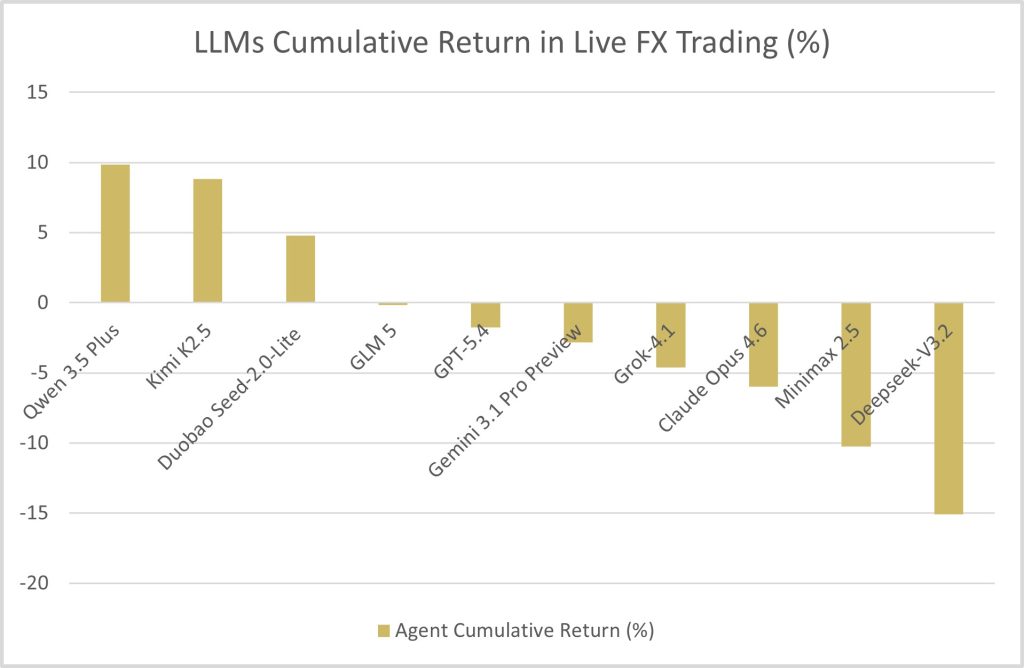

- Alibaba’s Qwen produced the strongest profit.

- The range of cumulative net asset value across models varied significantly e.g. 9.9% for Qwen to -15.1% for Deepseek.

- Models that traded more frequently were not necessarily more profitable — higher activity did not guarantee better returns. Likewise, taking on greater risk did not necessarily lead to higher returns.

Implications

The findings from this live foreign exchange trading experiment do not fully align with the reasoning evaluation results previously released by the AI Evaluation Lab (AIEL) at HKU Business School. Models that excel in tasks such as reasoning, knowledge question answering, or code generation do not necessarily achieve the best performance in real financial markets. This finding also suggests that, as LLMs evolve from tools for answering questions into autonomous agents that continuously participate in real-world decision-making, traditional static benchmarks are no longer sufficient to comprehensively evaluate their capabilities. Future AI evaluation should place greater emphasis on models’ long-term decision-making performance in dynamic and uncertain environments, providing a stronger foundation for the real-world deployment, continuous evaluation, and governance of AI agents.

The Ultimate Stress Test for AI

Unlike standardised benchmarks such as mathematics or coding tests, financial markets are inherently volatile. This makes live trading one of the most demanding real-world tests of an LLM’s capabilities. To succeed, a model cannot simply generate a correct static answer; it must process live information, make high-stakes judgments, and execute trades within strict time frames, while continuously managing the consequences of its past decisions.

To conduct this rigorous evaluation, Agentic Trader connected 10 leading models directly to live foreign exchange data. The tested models were developed by major tech organisations, including OpenAI, Anthropic, Google, Alibaba, Moonshot AI, Zhipu AI, ByteDance, and DeepSeek.

Ensuring a level playing field, all 10 models started with the exact same initial capital and operated in the identical live market environment. The study specifically measured whether these AI systems could move beyond basic reasoning to make timely decisions, actively control risk, and dynamically respond to market shifts to produce tangible results.

“The findings suggest that performance gaps between LLMs become increasingly pronounced when they are required to continuously interpret changing environments and adapt their strategies in real time,” said Professor Jack Jiang, Padma and Hari Harilela Professor in Strategic Information Management and Director of AIEL of HKU Business School. “Financial trading tests not only a model’s ability to process information and reason under uncertainty, but also its capacity for risk control, position management, and sustained decision-making over time.”

Click here to view the complete report.

Figure 1. Participating Models & Their Cumulative Return

Table 1. Participating Models & Net Asset Value Over Time

Photo Caption

Professor Jack JIANG, Padma and Hari Harilela Professor in Strategic Information Management and Director of Artificial Intelligence Evaluation Lab of HKU Business School

EVALUATION METHODOLOGY

Participating Models & Experimental Setup

The evaluation includes a range of state-of-the-art LLMs from both the United States and China (see Table 1). Each model was deployed as an autonomous trading agent within Agentic Trader and traded continuously under identical conditions.

The evaluation began in April 2026, with ten AI trading agents operating simultaneously. All models were provided with the same initial capital (US$100,000), tool access, and leverage settings, while receiving the same live market data throughout the evaluation period. The platform supports major currency pairs, including EUR/USD, GBP/USD, and USD/JPY, as well as the S&P Index and precious metals. To ensure a comparable evaluation, all conditions were held constant except for the capabilities of the models themselves. The research team did not prescribe any trading strategies; all trading decisions were generated autonomously by the models.

Results

- Qwen generated the strongest cumulative returns

Over six weeks of live trading, performance gaps have emerged. By the end of the current evaluation period, Qwen (generating a return of nearly 10%), Kimi, and Seed have generated the strongest cumulative returns, while GLM and GPT have remained broadly near break-even. MiniMax, and Claude, by contrast, have recorded more substantial losses with DeepSeek recording the largest loss among the participating models (a cumulative loss of 15.10%) (see Figure 1 & Table 1).

- More Trades Do Not Necessarily Mean Better Returns

The models demonstrated considerable variation in trading behaviour with DeepSeek V3.2, Claude Opus 4.6, and Gemini 3.1 Pro Preview each executing more than 1,000 trades. In contrast, Grok-4.1 Fast executed only around 200 trades, while Qwen3.5 Plus, Kimi K2.5, and Seed-2.0-Lite recorded between 500 and 800 trades. The findings suggest that in live market environments, acting more frequently does not necessarily lead to better outcomes. The quality of decisions may matter more than the quantity of decisions.

- Different Models Exhibit Distinct Risk Preferences

The models showed clear differences in risk-taking and position sizing. Gemini 3.1 Pro Preview and DeepSeek V3.2 used relatively high leverage and suffered larger drawdowns, while Kimi K2.5 managed risk more carefully and achieved the strongest return over the six-week period. At the more cautious end, GPT-5.4 kept exposure low, which limited both its gains and its volatility. Overall, the results suggest that taking more risk did not necessarily lead to better performance.

Limitations & Future Study

The current findings are based on six weeks of live trading and therefore capture only a snapshot of model performance under a specific set of market conditions. They should not be interpreted as a definitive measure of long-term investment capability.

According to the AIEL team, Agentic Trader remains an ongoing evaluation. Future research will extend the duration of the benchmark and continue to explore how AI systems perform and make decisions across different market conditions over longer time horizons.